The Lithuanian Investment Index for 2017 compiled by INVL Asset Management, one of the country’s leading asset management firms, shows shares of Lithuanian companies continued their victory march last year, outperforming the country’s other main asset classes. The return on stocks was 17%, while that on rental housing was 7.7%. Long-term Lithuanian bonds fell short of the country’s 3.7% inflation rate with a return of 0.4%, and for a second year in a row deposits gave no return. The return on housing prices, at 3.6%, was also less than inflation last year.

“Over the last decade returns on the country’s main asset classes have been uneven. After the financial crisis bonds and deposits were the better performers too, while during the last five years rental housing and Lithuanian shares have stood out as the two leading asset classes. Stocks have been in the top position for two years now,” said Vaidotas Rūkas, Head of Investment Management at INVL Asset Management.

In the past five years, stocks earned a higher annual return than the country’s other asset classes not just last year but also in 2013 (with 18.7%) and 2016 (with 14.9%), and only fell short of the return on rental housing investments in 2014-2015, when stock returns were a bit more than 7%. Returns on investments in rental housing during the past five years ranged from 6.4% in 2013 to 9.7% in 2016.

Looking at long-term trends, those who invested over the period 1996-2017 could have earned gains from all the asset classes, since their average annual returns were all positive and higher than Lithuania’s average inflation. Investments in rental housing had the biggest average annual return in this period, at 14.3%. Stocks returned 9.3%, long-term bonds 6.7%, housing prices 6.4% and deposits 4.8%. Results for the last 10 years (2008-2017), however, show that most of the asset classes being assessed for the country were impacted by the last economic crisis, with only Lithuanian long-term bonds outperforming inflation during this period.

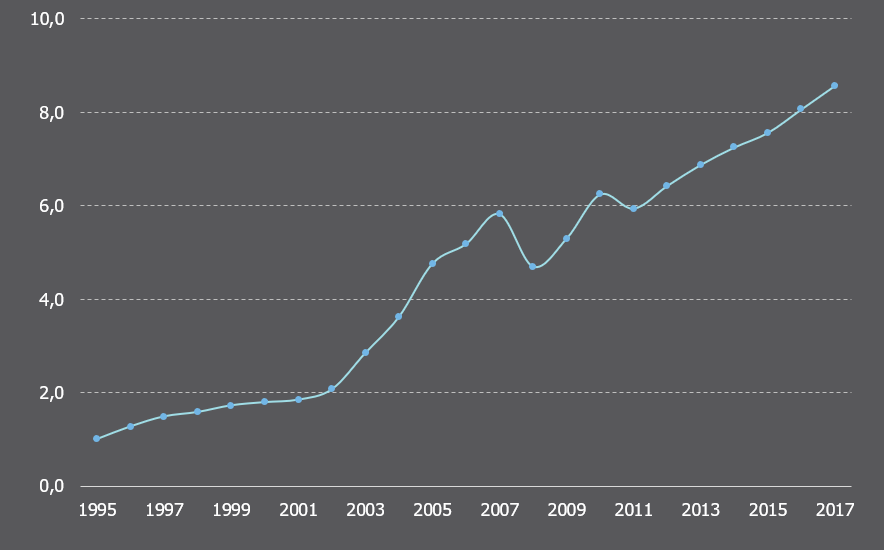

INVL Asset Management’s Lithuanian Investment Index gives equal weight to annual assessments since 1995 of returns on money market instruments (deposits), long-term Lithuanian bonds, rental housing (as of 2016 calculated net of expenses) and stocks. The index, which depicts investments in these Lithuanian asset classes, increased 6.3% in 2017 or a bit more slowly that in 2016 when it rose 6.7%. The somewhat smaller increase in the index was due to slower growth last year in the returns on bonds and rental housing. According to the index, the average annual return on investments in Lithuania was 10.3% for the period 1996-2017 and 3.9% for the most recent decade, and exceeded the return on many alternatives.

Lithuanian stocks outperformed European stocks

Lithuanian stocks, clearly standing out from the country’s other asset classes with a return of 17% in 2017, did better than European stocks last year but not as well as global stocks. Though for the last decade (2008-2017) the return on Lithuanian stocks was smaller than that on European and global stocks, for the past 22 years it was bigger. Rental housing had the second-best return among Lithuanian asset classes in 2017, at 7.7%, which was smaller than the 2016 figure of 9.7%.

Lithuanian long-term bonds had a return of 0.4% in 2017. That was less than U.S. 10-year bonds (2.8%) but more than German long-term bonds (-0.8%) which are considered the safest investment. For the period of the last 22 years, though, Lithuanian long-term bonds, with a gain of 6.7%, outperformed returns on U.S. and German bonds. For a second year in a row, deposits in Lithuania did not earn anything for their holders, continuing to lose part of their value due to inflation.

Growth expected from stocks

“What lets you get optimal results and the best return on investments is long-term investing, which neutralizes the fluctuations that are unavoidable over a long period. Over the long term the profitability of separate asset classes varies, but by suitably allocating investments among asset classes you can get the best out of investing,” Vaidotas Rūkas said.

A chance to diversify investments according to the desired level of risk is also offered by Lithuanian pension funds, in existence since 2004, which focus on long-term gains. Four categories of 2nd pillar pension funds operate in the market: equity, medium equity share, small equity share, and conservative investment pension funds. The average return they earn over different periods balances out among the grains on stocks and bonds in various regions. The average annual return on pension funds operating in Lithuania, since they were introduced in 2004, is 4.7%. For the period 2008-2017 it was 3.5%, and for the year 2017 it was 4.5%.

In forecasting future trends, Vaidotas Rūkas said potential gains could be expected from stocks or rental housing income. “Trends for Lithuanian bonds and deposits aren’t going to change anytime soon. It’s also hard to talk about housing prices rising, especially in Vilnius, as the market is now rather saturated, so there probably aren’t gains to be had in housing unless from rental income. Stocks, meanwhile, even if in the short run they have a tendency to fluctuate, over the longer term have good prospects given the strong economy and attractive valuations,” he said.

Number of employed people grew further and more earned higher pay

Long-term investments in Lithuania have been profitable, but what objective opportunities do residents of the country have to earn extra money by saving and investing? How has their income changed over the past year, how do they themselves see their financial situation, and how many of them are focusing on their long-term financial plans?

According to Statistics Lithuania, the number of employed people in the country rose to 1.22 million in 2017, up 3.4% since 2008 (fourth-quarter data) and nearly 12 500 more than a year earlier. The average monthly gross wage rose 7.5% last year to EUR 884.80 in the fourth quarter of 2017, though wage growth slowed from 8.7% in 2016. Between 2008 and 2017, comparing the last quarters, the average gross wage in the country increased by EUR 213.10 or 31.7%.

One positive trend last year was a decrease in the number of people earning a monthly wage of EUR 400 or less and an increase in the number earning more. According to state social insurance fund data, the share of employed persons earning EUR 400 or less shrank to 17% in January this year from 27% in January 2017. Those earning EUR 401-700 made up the largest portion of employed persons, at 37% (versus 33% in 2017), while those earning EUR 701-1000 comprised 21% (19% in 2017), those earning EUR 1001-2000 made up 20% (17% in 2017), and those earning EUR 2001 or more accounted for 5% of employed persons (4% a year earlier).

Residents’ financial assets also increased rather significantly. According to information published by the Bank of Lithuania, the liquid financial assets of the country’s households (cash and deposits, life-insurance and annuity commitments, mutual funds, pension funds, debt securities and loans, and listed shares) grew to EUR 18.8 billion in the third quarter of 2017, up from EUR 17.2 billion in the same period of 2016 and EUR 10.7 billion in 2008.

The largest portion of such assets are still held in cash and deposits: 71% last year, versus 72% in 2016 and 81% in 2008. Meanwhile, few venture to invest in financial instruments providing a higher return, with the proportion of such persons little changed. An exception is pension funds, which are the financial instrument that grew the most over the past decade as their share of households’ liquid financial assets increased from 6% in 2008 to 15% last year.

“Changes in the portfolio of residents’ asset since 2008 show that what has grown most is the proportion of money in pension funds, the use of which for long-term saving the state also encourages. Surveys show that future expectations related to pension funds are also increasing: considering their plans for the future, this year there was an increase in the number of people who plan to support themselves in retirement with pension fund pay-outs,” said Dr Dalia Kolmatsui, Head of Pension Funds & Retail at INVL Asset Management.

Pension expectations are falling even as retirement needs remain high

A representative survey of Lithuanian residents conducted for INVL Asset Management by Spinter Tyrimai in February 2018 revealed that 88% of respondents expect to live off state social insurance (Sodra) pension payments when they retire, up from 83% the year before last. The share of respondents who expect to support themselves with pay-outs from pension funds, meanwhile, rose to 41% (from 36% in 2016), and the proportion of those who plan to work during retirement increased to 22% (from 17% in 2016). Among the respondents, 32% indicated savings as a source of income in retirement (21% in 2016), and 8% indicated real estate they own (11% in 2016).

The increase in those who expect to support themselves with pension fund pay-outs may be due to the fact that people’s retirement needs grew during the year, according to Dr Kolmatsui. “Almost half of respondents hope to get the same income in retirement as they do now, while 29% hope for 75% of their current income, for quality of life after they stop working. You can try to meet such high expectations, but it requires saving additionally for retirement,” she stressed.

Dr Kolmatsui said it seems ever more people in the country realize that saving additionally for retirement is essential. “The survey shows that residents’ expectations about the pension they’ll get fell during the year, and nearly a third now think that in retirement they’ll only get half their current income,” she said. Among respondents, 29% said they think they will receive a pension that is 50% the size of their current income (versus 23% last year). The proportion expecting a pension equal to 75% of their current income fell from 20% last year to 12% this year, while those expecting a pension at the same level as their current income fell from 13% last year to 10% this year.

People’s financial position most often helped by higher wages, hurt by rising prices

In assessing their financial situation, Lithuanian residents are somewhat more positive than they were last year, though there remains a significant number whose situation has worsened mainly due to increased prices. According to the survey’s results, 34% said their financial situation improved over the last three years (versus 29% last year), while 50% said it worsened (56% last year).

As reasons why their financial situation improved, this year a remarkable 70% of respondents indicated increased wages (versus 58% in 2017), while 44% said that another family member got a job or higher pay (33% in 2017).

As reasons why their financial situation worsened, a full 67% said prices increased while their income did not change (62% gave that reason last year) and 22% said their income increased but prices rose even more (18% last year). This year 29% said that their income was unchanged but their needs increased, a reason given by 13% last year.

The proportion of respondents who could live off their savings for up to one year without changing their normal way of life decreased to 7% this year, from 11% in 2016. Those with sufficient funds to live for up to half a year at the same standard of living increased this year to 23% (from 17% in 2016), and the share who said they could do so for up to three months was 53% this year and last year, compared with 57% two years ago.

“The survey shows that if they lost their income, more than half of people only have enough savings to maintain their standard of living for up to three months. That’s one more strong reason why financial planning is essential. It lets you not just create your own sources of income for the future, but also arrange for the financial stability of your family in unexpected situations,” Dr Kolmatsui stressed.

Dr Kolmatsui noted that there is some good news regarding trends in financial planning among people in Lithuania. According to this year’s survey, the proportion of those with a financial plan for themselves or their family increased from 15% to 23%. Still, most of them only plan for periods of up to two years (30% of those with a plan) or five years (28%), while 15% have a plan for up to ten years and 17% for more than ten years.

INVL Asset Management is part of the Invalda INVL group whose companies manage pension and mutual funds, alternative investments, private equity assets, investment portfolios and other financial instruments. Over 185 000 clients in Lithuania and Latvia and international investors have entrusted them with more than EUR 575 million of assets.

Lithuanian Investment Index

Return by class of Lithuanian assets

| Asset class* | 1996-2017 average return, % |

2008-2017 average return, % |

2017 return, % |

| Rental housing (net of expenses starting in 2016) | 14.3 | 1.2 | 7.7 |

| Housing prices in Lithuania | 6.4 | -3.7 | 3.6 |

| Lithuanian stocks | 9.3 | 2.4 | 17.0 |

| Short-term debt securities and money market instruments (deposits) | 4.8 | 2.1 | 0.0 |

| Lithuanian long-term bonds | 6.7 | 4.2 | 0.4 |

| 2nd pillar pension funds | 4.7** | 3.5 | 4.5 |

| Inflation | 3.3 | 2.8 | 3.7 |

| Lithuanian Investment Index | 10.3 | 3.9 | 6.3 |

* Housing acquisition and rental returns calculated on the basis of Ober-Haus data.

** Since creation in 2004.

Information is provided for information purposes and cannot be construed as a recommendation, offer or invitation to invest in funds operated by INVL Asset Management or other financial instruments. When investing, you assume the investment risk. Investments can be both profitable and loss-making, you may not obtain financial benefits and you may lose some or even all of the invested amount. Past results of investments do not guarantee future results. When making a decision to invest, you should assess all the risks associated with investing and the key investor information documents. INVL Asset Management shall not be responsible for any inaccuracies or changes in this information or for losses that may arise when investments are based on this information.