It paid off to invest in Lithuania over the past 20 years – investments in the country’s main asset classes over the period earned an average return higher than inflation and were profitable, with rental housing and stocks performing best while deposits provided the smallest return. For the 10-year period 2006-2015, which was impacted by the global financial crisis, long-term bonds delivered the highest average return on investments in Lithuania, while purchased housing in the country had the lowest return. Long-term bonds and pension funds outperformed inflation in this period.

These are among the insights confirmed by the first-ever calculation of the Lithuanian Investment Index, presented by INVL Asset Management, one of the country’s leading asset management firms.

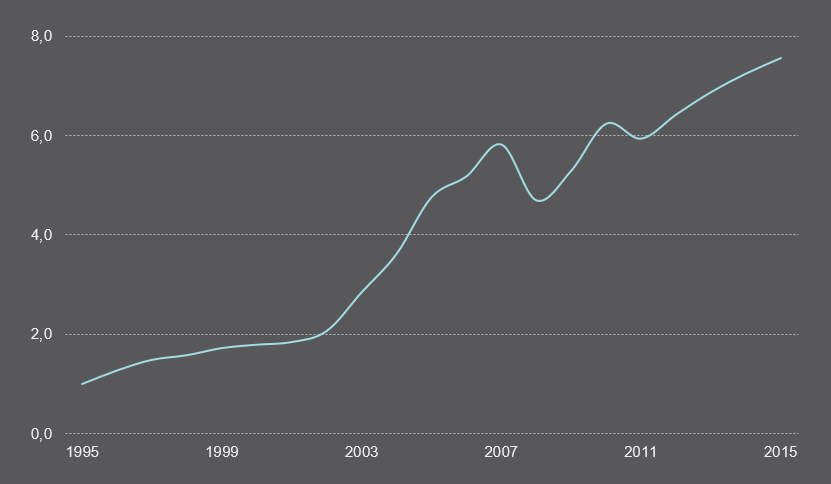

The index shows that the average return on investments in Lithuania in 2006-2015 was 4.7 per cent and exceeded the return on many analysed investments, while for 1996-2015 the figure was an impressive 10.6 per cent, confirming the benefits of long-term investments. In 2015, the investments in Lithuania with the highest return were the country’s stocks and rental housing (excluding costs), while those with the lowest were deposits, which had a return equal to zero. The Lithuanian Investment Index is composed of equal proportions of money market instruments (deposits), long-term bonds, rental housing (disregarding costs) and stocks.

Though only some people invested, assets grew

“While it’s been possible to invest for more than 20 years now in Lithuania, investment traditions in the country are still just taking shape. The accumulated assets of the country’s residents are growing, as are the amounts allocated for investment, but most money is still being held in deposits and cash. Our goal in preparing the first Lithuanian Investment Index was not just to survey the main asset classes and their yields, but also to provide an assessment of the return on investing in Lithuania,” said Vaidotas Rūkas, Chief Investment Officer at INVL Asset Management.

Bank of Lithuania data show that the liquid financial assets* of the country’s residents grew 4.5 times in 2003-2016 to EUR 17.3 billion as of the middle of this year, while assets per capita increased 5.5 times to EUR 6,000. Residents have invested ever more money over the last two decades, and in mid-2016 funds entrusted to management by professionals totalled EUR 3.69 billion.

The largest amount, EUR 2.31 billion, was held in pension funds, which have operated since 2004, while EUR 0.98 billion was invested in insurance and annuity products in 2016 and EUR 398.6 million was invested in mutual funds. Still, Lithuanian households’ share of mutual fund assets in 2014 was only 1.2 per cent, compared to figures of more than 10 per cent in Belgium, Luxembourg, the USA, Spain, and Hungary.

“Although the country’s residents are allocating more and more money to investments, the proportion of cash and deposits in their financial portfolio remains quite high, at 70 per cent. So far, then, we’re lagging well behind countries that have deep investment traditions,” Rūkas noted. On the other hand, a review of investments for the last two decades shows this period could have been lucrative.

Investments secured gains over the past 20 yeas

“The Lithuanian Investment Index makes it possible to assess the return on specific investments over the period 1996-2015. For instance, if 1,000 euros in 1996 were allocated in equal parts to investments in Lithuanian stocks, bonds, money market instruments and rental housing disregarding expenses, at the end of the period that investment portfolio would have been worth 7,565 euros,” Rūkas explained.

He pointed out that the return on specific classes of assets is different in different periods, so spreading investments over a variety of areas is recommended in order to reduce risk and sustain gains. He noted that returns on investments in residential property are tied to specific traits of each market, and this market in Lithuania has been extremely volatile.

“The period 1996-2005 was profitable, but over the past decade the return on purchasing residential property was actually negative and the only gains from the renting out of housing. Short-term advances in the housing market in Lithuania have been influenced largely by housing credit expansion, while long-term increases reflect people’s increasing purchasing power. Meanwhile, housing markets in countries like Germany, the UK or the USA have gone their own ways – in Germany housing prices have stayed at similar levels over the last 20 years, in the USA they’ve risen at a rate similar to inflation, and in the UK housing prices have risen extremely rapidly,” Rūkas said.

Stocks have been volatile, bonds met expectations

The return on Lithuanian stocks has been rather erratic. For 1996-2015, it was 8.7 per cent and exceeded the returns on European and global equities, but in 2006-2015 it was lower, at 0.8 per cent. The main factor during that decade was the financial crisis, which in 2008 alone erased 65 per cent of stocks’ value.

Pension funds, which are the most popular form of investment in Lithuania, earned a 4.9 per cent average annual return from their creation in 2004 through 2015. For 2006-2015, the return was 3.5 per cent, which was higher than both inflation and the return on stocks.

Looking at yields on safe investments – bonds and deposits – in Lithuania, the USA and Germany, the best performers over the last 20 years were Lithuanian long-term bonds, which returned 7.3 per cent. In the most recent decade, though, German long-term bonds performed best, yielding 5.5 per cent. Nonetheless, bonds are currently seen as essentially the only asset class for which it’s not possible to predict similar historical returns over the short-term and medium-term.

For optimal results, spread investments out

“The index of investment returns clearly shows that long-term investing enables you to avoid possible bigger fluctuations in investment returns, and that a properly formed investment portfolio, with funds allocated to diverse asset classes, makes it possible to get an optimal return. But the most important thing is simply to take advantage of investment opportunities and the potential return they offer, since historical results both in Lithuania and the world demonstrate the benefits of doing so,” Vaidotas Rūkas said in summary.

INVL Asset Management is part of Invalda INVL, one of the Baltic region’s leading asset management groups. Companies in the group manage pension and mutual funds, alternative investments, private equity assets, individual portfolios and other financial instruments. They have been entrusted with managing over 400 million euros of assets by more than 170,000 clients in Lithuania and Latvia as well as international investors.

*Liquid financial assets of the country’s residents include cash and deposits, life and non-life insurance and annuities, mutual funds, pension funds, debt securities and loans, and listed shares. Source: www.lb.lt: Financial assets of institutional sectors (S14+S15 Households and NPI serving households)

Supplementary information

Lithuanian Investment Index

Average return by asset class

| Asset class | 1996-2015 average, per cent |

2006-2015 average, per cent |

2015 average |

| Housing prices and rental income (excluding expenses) | 14.8 | 4.8 | 7.9 |

| Housing prices and rental income (net of expenses) | 12.8 | 2.8 | 5.9 |

| Housing prices in Lithuania | 6.6 | -0.3 | 2.3 |

| Lithuanian stocks | 8.7 | 0.8 | 7.4 |

| European stocks (EUR) | 7.8 | 5.3 | 10.3 |

| Global stocks (USD) | 6.6 | 5.7 | 1.8 |

| Lithuanian long-term bonds | 7.3 | 4.2 | 1.9 |

| US 10-year bonds | 5.4 | 4.7 | 1.3 |

| Short-term debt securities and money market instruments (deposits) |

5.3 | 3.0 | 0.0 |

| Gold (USD) | 5.2 | 7.5 | -10.6 |

| 2nd pillar pension funds | 4.9** | 3.5 | 3.6 |

| Inflation | 3.4 | 3.4 | -0.7 |

| Lithuanian Investment Index | 10.6 | 4.7 | 4.3 |

**since creation in 2004

Any use of data herein must identify INVL Asset Management as the source.